Page 76 - ID - Informazioni della Difesa n. 03-2025 - Chiuso

P. 76

MITIGARE I CONFLITTI FUTURI: COOPERAZIONE interruzioni commerciali. Diversificare le catene di

INTERNAZIONALE E ALTERNATIVE approvvigionamento sviluppando nuovi progetti

Sebbene il potenziale di conflitti futuri per le terre rare minerari, incoraggiando iniziative di riciclo e

e le materie prime critiche sia significativo, esistono investendo in fonti alternative di terre rare può

diverse strategie che le nazioni possono perseguire ridurre queste vulnerabilità e garantire una fornitura

Besides highlighting the forecasted EU demand in 2030 relative to current production, the figure shows that the

per mitigare questi rischi e garantire una distribuzione più stabile di materiali critici. Access to raw materials and EU strategic partnerships

ERMA cases identified to date can supply a very significant proportion of the EU demand. The values reported

più stabile ed equa di queste risorse vitali. Il primo passo verso la diversificazione è lo sviluppo In recent times, raw materials have forcefully come to the attention of the public and policymakers. There is now

in Figure 2 are based on the current assumptions in terms of relative proportions of energy sources and battery

Una delle strategie più efficaci è la diversificazione di nuovi progetti minerari in regioni precedentemente an increased awareness of the risks associated with potential disruptions in the supply chains that underpin the

delle catene di approvvigionamento globali. sottoutilizzate. Paesi come Australia, Canada e nazioni EU’s economic prosperity, social stability and safety.

types, as outlined in Figure 3. Figure 4 further shows that ERMA investments are distributed not only across Eu-

Attualmente, la produzione e la raffinazione delle africane detengono riserve significative di terre rare e

rope and among different materials, but also, most importantly, across value chains. This is in line with ERMA’s

terre rare sono altamente concentrate in alcune altre materie prime critiche, ma queste risorse non sono

strategy to build up capacity and skills across all stages of the value chain, from exploration to mining, process-

regioni chiave, in particolare in Cina, che controlla state pienamente sfruttate a causa della mancanza While it is true that significant capacity exists within the EU, international partnerships need to be further de-

ing, manufacturing and recycling. More investment cases will be submitted to ERMA in the coming months and

una parte significativa del mercato globale. Questa di investimenti o infrastrutture. Collaborando con veloped to ensure diversification of supply and to address short-term as well as long-term gaps for some ma-

years, potentially increasing the overall materials for energy storage and conversion production and recycling

concentrazione dell'offerta ha creato vulnerabilità queste nazioni per sviluppare progetti minerari, i terials. International partnerships need to be developed in harmony and synergy with the support provided by

capacity in Europe across the various CRMs value chains.

per le nazioni che dipendono da questi materiali, paesi che attualmente dipendono dalle importazioni the EU and Member States to develop domestic resources. In this context, ERMA is multiplying its international

in particolare in caso di tensioni geopolitiche o cinesi possono ridurre la loro dipendenza da un strategic partnerships and outreach activities, both in terms of membership and in the leadership of investment

cases (Figure 5). In line with the European Commission’s outreach strategy, ERMA is a key player in the part-

Graphite nership with Canada and has been a driving force in the Memorandum of Understanding between the European

LCE Union and Ukraine on a Strategic Partnership on Raw Materials. Other non-EU countries of strategic relevance

NMC Mn for ERMA include Kazakhstan and Namibia, and several countries with partnerships in the pipeline (Greenland

Battery Production Co

Ni and Norway) or already announced (Argentina, Australia, Chile, Democratic Republic of Congo and Rwanda).

NCA

LFP Besides its industry support for individual investment cases, ERMA is assisting the European Commission with

Si the identification of emerging technologies and research topics that will restore the EU’s know-how and inno-

vation capacity. These include, among others, exploration, mining, processing, and recycling of materials used in

PV Solar Production

solar energy, wind energy and hydrogen-related technologies.

Cu

Wind Generator Production

Zn

Cr

REE

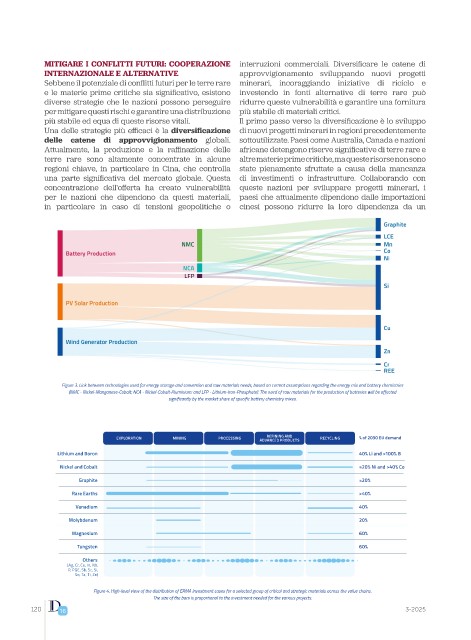

Figure 3. Link between technologies used for energy storage and conversion and raw materials needs, based on current assumptions regarding the energy mix and battery chemistries

(NMC - Nickel-Manganese-Cobalt; NCA - Nickel-Cobalt-Aluminium: and LFP - Lithium-Iron-Phosphate). The need of raw materials for the production of batteries will be affected

significantly by the market share of specific battery chemistry mixes.

Greenland

REFINING AND

EXPLORATION MINING PROCESSING ADVANCED PRODUCTS RECYCLING % of 2030 EU demand Norway Kazakhstan

Lithium and Boron 40% Li and >100% B Canada Ukraine

Nickel and Cobalt ≈20% Ni and >40% Co

Graphite ≈20%

Rare Earths >40%

DRC Rwanda

Vanadium 40%

Namibia

Molybdenum 20% Australia

Magnesium 60% Chile

Argentina

Tungsten 60%

Others Partnerships Signed Partnerships in the pipeline Partnerships Announced

(Ag, Cr, Cu, In, Nb,

P, PGE, Sb, Sc, Si,

Sn, Ta, Ti, Zn)

Figure 4. High-level view of the distribution of ERMA investment cases for a selected group of critical and strategic materials across the value chains. Figure 5. Current and future EU-International strategic partnerships in the raw materials sector. Source: European Commission.

The size of the bars is proportional to the investment needed for the various projects.

120 16 3-2025 17